Tender Offers: The New Engine of Venture Liquidity

Insights from Fabrica Ventures Team.

Even Benchmark Goes Late-Stage

June 5, 2026

Our St. Patrick’s Day

June 21, 2026

The past several years have legitimized venture secondaries as startups stayed private longer and traditional exits became increasingly scarce.

What was once viewed as a niche corner of VC has become a core part of how capital is raised, allocated, and returned. Venture secondaries are no longer cyclical — they are structural.

In 2025 alone, more than $100B of private-company shares changed hands through secondary transactions in the US. The secondary market has reached a scale comparable to both the IPO and M&A markets.

Historically, the most common secondary transactions were one-off sales by employees seeking liquidity. But as competition for talent intensifies — particularly in AI — liquidity has become an increasingly important recruitment and retention tool.

After all, nearly half of today’s unicorns are more than nine years old. Many early employees and investors have been waiting a decade or more for a meaningful liquidity event.

As a result, company-sponsored tender offers have become increasingly common.

Unlike ad hoc secondary transactions, tender offers provide employees and early investors with a structured and predictable path to monetize part of their holdings. Because these transactions are organized by the startup itself, management retains greater control over pricing, participant eligibility, transaction size, and cap-table composition.

Tender offers are also frequently conducted alongside primary financing rounds, creating a transparent market-clearing price that aligns the interests of buyers, sellers, and the company.

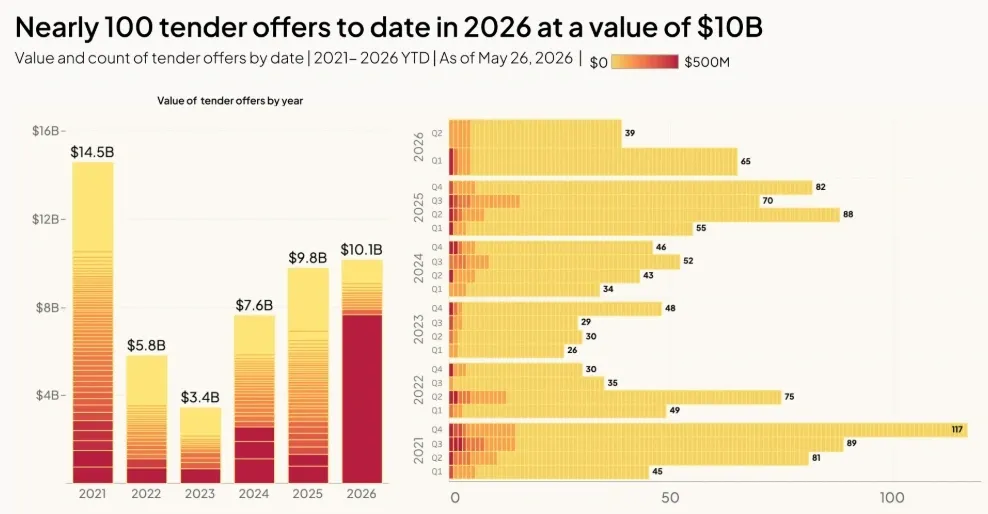

The trend is accelerating.

Tender-offer volume reached $10.1B by May 26, 2026—already exceeding the full-year totals of 2022 ($5.8B), 2023 ($3.4B), 2024 ($7.6B), and 2025 ($9.8B). If current activity continues, 2026 could surpass the previous record of $14.5B set in 2021.

Conclusion

Tender offers are becoming an increasingly important source of liquidity in VC. Participating in tender offers typically requires established relationships, continuous monitoring of the secondary market, and sufficient scale to transact when opportunities arise.

The growing importance of tender offers is one of the trends that highlights the value of a dedicated secondary-market vehicle such as Fabrica Ventures Fund III.

{kind=link}

{kind=link}

{kind=link}