DPI: The Metric That Matters While a Fund Is Alive

Insights from Fabrica Ventures Team.

The Real Signal Behind CNBC’s Disruptor 50

May 24, 2026

Even Benchmark Goes Late-Stage

June 5, 2026

There are several ways to measure VC fund performance.

Once a fund is fully realized, Net IRR is arguably the most informative metric because it captures both the magnitude and timing of returns.

But what is the best metric while a fund is still alive?

For years, VC managers highlighted unrealized portfolio marks. Increasingly, however, LPs are paying attention to a much simpler question:

How much cash has actually come back?

Wall Street is slowly reaching the same conclusion. A recent article in The WSJ captured the shift perfectly:

“Private Equity’s Exit Drought Claims Its Latest Victim—the IRR Metric. Internal rate of return, a much-used performance yardstick, is losing its cachet as investors focus on cash distributions from funds.”

The reason is straightforward. Unrealized valuations can fluctuate, assumptions can change, and paper gains may never materialize. When the IPO window shut, VC discovered the difference between marks and money. Many private-company shares began trading in the secondary market at discounts of 40% or more to their last funding-round valuations. Fortunately, the rise of secondaries provided a release valve, accounting for roughly one-third of venture-backed liquidity events in recent years.

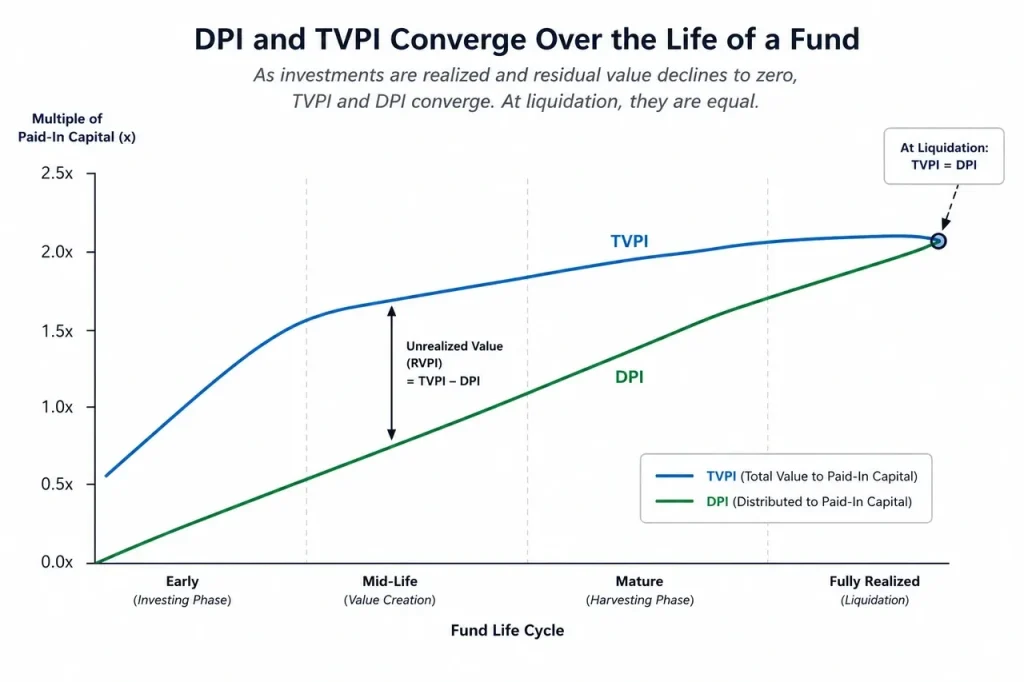

This distinction is reflected in two of the industry’s most widely used metrics. TVPI (Total Value to Paid-In Capital) measures the sum of realized distributions and unrealized portfolio value relative to invested capital. DPI (Distributed to Paid-In Capital) measures only the cash actually returned to investors relative to invested capital.

In the end, TVPI is a valuation. DPI is cash. LPs can spend and recycle cash.

Conclusion

We have always emphasized the importance of DPI to our LPs.

According to Carta, Fabrica Ventures Fund I (2020 vintage) ranks in the top quartile for DPI, while Fund II (2023 vintage) ranks in the top decile, among more than 2,700 VC funds.

Importantly, Fund I, while already ranking in the top quartile for DPI, still holds positions in three companies that have already gone public. We continue to hold Omada Health and Netskope and are awaiting the expiration of Cerebras’ lock-up period. In other words, the fund’s current DPI ranking reflects only part of the story.

As we prepare to launch Fund III, the lessons from Funds I and II remain unchanged: realized distributions matter.

Because, in the end, cash is reality. Everything else is an estimate.

{kind=link}

{kind=link}

{kind=link}