The Welcomed Venture Growth Stage

Insights from Fabrica Ventures Team.

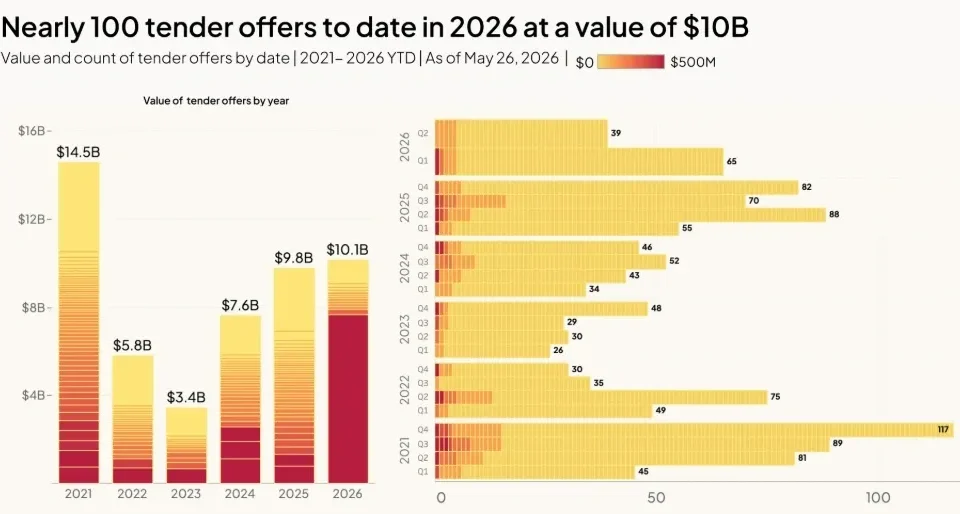

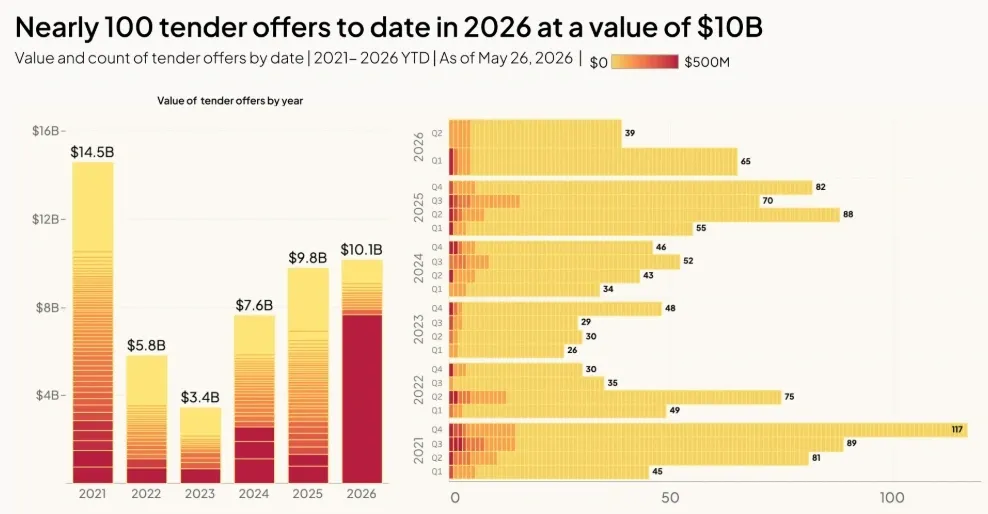

Startup-to-startup M&A

November 26, 2022

Are Insider-Led Rounds Good or Bad?

December 11, 2022

All figures from PitchBook.

Traditionally, the VC market is segmented in three: Angel & Seed, Early Stage and Late Stage.

Late Stage is by far the largest segment in the US, representing around 65% of the capital invested ($237B in 2021) and 30% of the deal count (18K in 2021, in parity with Early Stage).

Moreover, the broader change that has happened in the US VC market since the global financial crisis of 2008 has come from Late Stage.

The Jumpstart Our Business Startups (JOBS) Act, turned into law in 2012, increased the maximum number of shareholders in a private company from 500 to 2,000. This change was key in allowing startups to grow to a much larger size with private backing. Because of this, more capital started pouring into US Late Stage and, indeed, US VC has outperformed other private investment strategies, with seven of the past 10 fund vintage years leading all other private strategies. Moreover, nontraditional investors, such as hedge funds, mutual funds, and sovereign wealth funds, could not stay out and also poured capital into the VC asset class.

By definition, Late Stage is composed of Series C or later startups. However, given the skyrocketing growth of the US Late Stage, this segment started mixing bananas with oranges. In 2021, for instance, the top-decile Late Stage valuation in the US reached $1.4B while the bottom-decile Late Stage valuation hit $15M. In addition, the dollar failure rate (risk / reward profile) of a Series F investment is less than half of a Series C investment.

So, to better assess these changes in Late Stage, Pitchbook created a new category named “Venture Growth Stage”, defined as:

* Rounds tagged as Series E+ or

* Deals involving companies that are at least seven years old and have raised at least six VC rounds

Companies that met these criteria in 2021, such as Turo, TripActions and ServiceTitan, accounted for 26% of all US VC dollars ($94B) and close to 5% of the US VC deals. Therefore, while capturing just a small portion of the overall market, “Venture Growth” holds profound weight.

From now on, PitchBook will adopt the “Venture Growth Stage” in its VC reports, which should add new important insights.

Conclusion

Given the “gray-hair” profile of our investors, since its inception Fabrica Ventures looked for the best risk / reward investment ratio given by the “Venture Growth Stage”. In fact, and avoiding decacorns, out of the 26 Fabrica Ventures Fund I portfolio companies only five are not in Series E+ and only four are below 7 years old.

{kind=link}

{kind=link}