Three Sequential Shocks Hitting Tech

Insights from Fabrica Ventures Team.

Defense, Rewritten by AI: Shield AI’s Software-Defined Platform

April 6, 2026

Fund III’s Analytical Edge: Fabrica Ventures and Sacra

April 16, 2026

2026 began with high expectations for a reopening of the IPO window — “IPO markets look primed to accelerate in 2026,” PwC, Dec 12, 2025 …

… Reinforced by AI momentum — with 93% of global AI VC funding in 2025 concentrated in the US — and by a massive backlog of IPO-ready companies, representing over $2.0T in unrealized VC value.

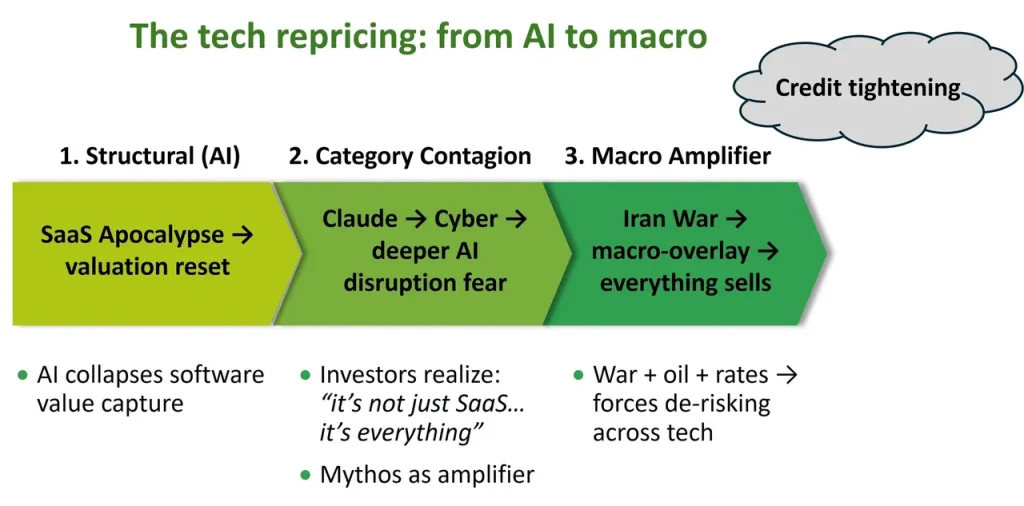

But three sequential “shocks” have repriced tech in 2026 in a profound way:

1. “SaaS Apocalypse” — AI attacks the application layer (Late Jan → Late Feb)

* Trigger: rapid releases from Anthropic’s Claude (Cowork, Agents, Code, plugins)

* Market reaction: $285B wiped in a single day across software & adjacent sectors; 27% drawdown in software ETFs since Jan

* Narrative shift: AI agents can replace workflows, not just assist; SaaS increasingly viewed as “overpriced middleware”

* First-order shock: AI compresses SaaS margins → multiple compression

2. Claude AI — Cybersecurity shock (Late Feb → Late Mar)

* Trigger: Expansion of Claude into security + vulnerability detection

* Market reaction: $14.5B wiped from cyber stocks in a single day

* Narrative shift: AI doesn’t just disrupt SaaS → it automates security itself

* Second-order shock: AI moves from replacing apps → replacing entire categories (cyber tooling)

And an additional layer, the launch of Claude Mythos in early April amplified the cyber shock narrative — accelerating the repricing beyond fundamentals.

3. Iran War — Macro + liquidity shock (Late Mar→ ongoing)

* Trigger: escalation of US/Israel –Iran conflict

* Market reaction: Nasdaq enters correction territory; broad-based tech sell-off

* Transmission channels: Oil ↑ → inflation fears; Rates ↑ → pressure on long-duration tech; Risk-off sentiment

* Third-order shock: Macro + geopolitics override fundamentals

And the cherry on top: at the same time, credit became more expensive and selective — with NAV loans and fund-level leverage slowing materially.

Conclusion

Markets always surprise — but the scale and depth of these three sequential shocks have been unprecedented.

{kind=link}

{kind=link}

{kind=link}