The Curious Case of Plaid’s Journey

Insights from Fabrica Ventures Team.

How to Control Enterprise AI Roadmaps

February 28, 2026

After Palantir, Anduril

March 13, 2026

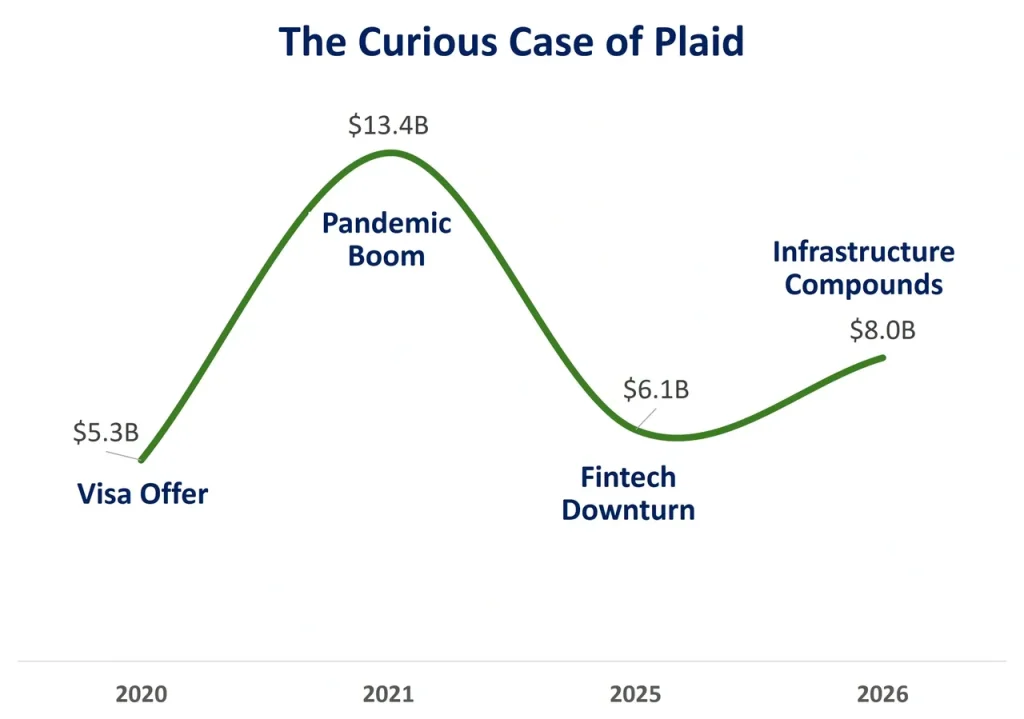

Plaid is the fintech infrastructure company most people never see — yet almost every fintech depends on it. Its APIs connect bank accounts to applications like Coinbase, Robinhood, Venmo and thousands of other financial services.

Plaid’s valuation history captures the turbulence of the fintech cycle over the past decade.

In 2020, the company appeared headed for a landmark exit when Visa agreed to acquire Plaid for $5.3B. But regulators blocked the deal on antitrust grounds, forcing Plaid to remain independent.

The timing turned out to be fortunate — at least temporarily.

In April 2021, during the peak of the pandemic funding boom, Plaid returned to the private markets and raised capital at a $13.4B valuation, one of the most prominent fintech rounds of the cycle.

The subsequent fintech downturn sent valuations tumbling across the sector. In April 2025, Plaid quietly raised capital at a $6.1B valuation — a painful 54% haircut from its 2021 peak, reflecting the broader market reset.

Yet the company kept building. Plaid expanded well beyond account linking, moving into identity verification, fraud prevention, and income verification — higher-margin infrastructure products that deepen its role in the fintech stack.

Fabrica Ventures has long liked Plaid’s fintech infrastructure play. And then, last year, we were able to invest in the company at more than a 20% discount to the down-round valuation.

Then, last week, Plaid marked a new milestone: an $8B valuation through an employee secondary sale — a 31% increase from its April valuation.

That $8B price tag suggests the market believes Plaid has regained its footing. The company processes billions of financial data connections each year, giving it unmatched scale in an infrastructure layer that becomes more critical as embedded finance spreads across the economy. Every neobank, lending platform, and investment app ultimately needs the plumbing Plaid provides.

Conclusion

Plaid’s $8B secondary valuation is more than a comeback story. It signals that infrastructure platforms with real revenue and defensible moats can still command strong valuations, even after the broader fintech correction.

Institutional buyers increasingly view the API layer as essential financial infrastructure — the plumbing of a system that is becoming more digital every year.

If the trend continues, the public markets may soon rediscover the value of fintech infrastructure.

{kind=link}

{kind=link}

{kind=link}