PE and Caesar’s Wife

Insights from Fabrica Ventures Team.

No Crystal Ball Required: VC 2026

January 5, 2026

Este Fundo Brasileiro Está Surfando a Onda de IPOs nos EUA

January 15, 2026

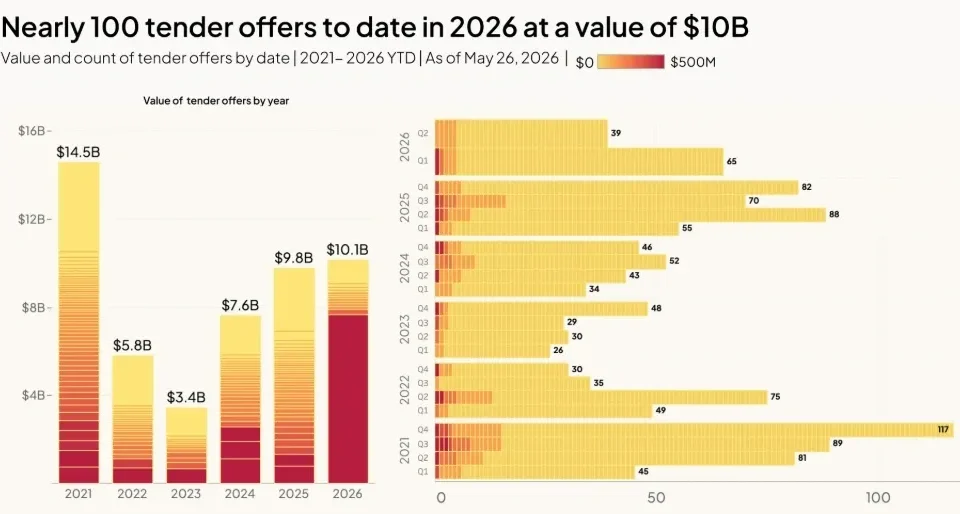

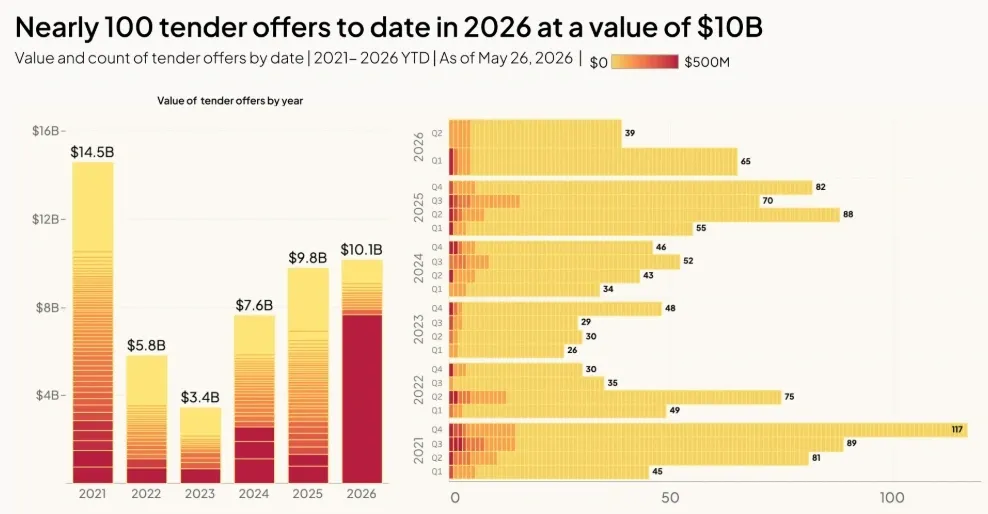

In the US, the PE (or LBO) asset class is over three times larger than VC in terms of dry powder. Structurally, PE targets mature, low-growth, cash-producing businesses using significant leverage — typically financing roughly 45% of the purchase with debt — while VC backs high-growth, loss-making technology startups almost entirely with equity.

PE is a thriving industry in the US. According to PitchBook’s 2025 data, PE investors deployed over $1.1T across more than 9,000 deals, marking the second-highest year of deal activity on record.

But these impressive deployment figures mask a growing structural concern. Last week, the Financial Times published an article titled “Private equity firms sell assets to themselves at a record rate,” highlighting a practice that increasingly resembles Ponzi-like dynamics: in 2025, roughly 20% of all PE exits involved firms raising fresh capital from new investors to purchase portfolio companies from their own aging funds.

According to Raymond James, this represents a sharp increase from the 12-13% observed in prior years, amounting to a staggering $107B in such recycled transactions in 2025.

This surge has been driven by so-called “continuation vehicles,” which allow large PE firms to provide liquidity to LPs in older funds while retaining control of the underlying assets — and, crucially, resetting the clock on management fees and carried interest — often with the same PE firm effectively sitting on both sides of the transaction.

The FT notes that this continuation-fund practice now extends to many of the industry’s most prominent firms: “PAI Partners flipped part of its stake in ice cream giant Froneri (think Häagen-Dazs) to a continuation vehicle for the second time in a €15 billion-valued deal. Vista Equity, New Mountain Capital, and Inflexion all deployed multibillion-dollar continuation funds to cling to their crown-jewel investments rather than face the harsh light of public markets or genuine third-party buyers”.

Some cases have even spilled into court. The Abu Dhabi Investment Council sued Energy & Minerals Group over an alleged undervalued self-sale of gas driller Ascent Resources; the deal collapsed, and outside bidders are now circling.

Conclusion

From a PE outsider’s perspective, VC transactions look more like Caesar’s wife — above suspicion.

{kind=link}

{kind=link}